Shariah-Compliant Banking Software Development

Learn how to develop a fintech app for a particular area with cultural variations and stringent regulatory standards.

The statistics speak for themselves: Islamic finance is outpacing traditional banking in numerous markets, driven by a vast, underserved demographic of Muslims seeking modern digital tools that align with their religious convictions.

For CTOs and product leaders, this landscape can seem daunting. You cannot simply rebrand an existing core banking system as "Halal" and expect it to function. That approach is fundamentally flawed. Instead of charging fees for lending capital, you must engineer systems based on risk-sharing and asset-backed structures, such as Murabaha or Musharakah.

The real hurdle lies in making these intricate profit-sharing calculations feel as seamless to the user as a standard wire transfer. Initially, it is frustrating to discover that off-the-shelf libraries for typical fintech platforms are incompatible, but teams eventually adapt to these unique constraints.

This guide will explore the essentials of building Shariah-compliant software. We will examine the critical features that define authenticity—because users can easily detect superficial compliance—and dive into the specific architectures and technology stacks required for this domain. Finally, we will address the inevitable regulatory complexities.

Defining Shariah-Compliant Banking Software

To a developer accustomed solely to Western financial institutions, this might appear to be a standard application with added filters. However, the reality is far more profound.

This software serves as the digital foundation for Islamic financial entities. It is a comprehensive ecosystem engineered to ensure that every data point and algorithmic decision adheres strictly to Islamic law (Shariah).

The stakes here are uniquely high. In conventional systems, compliance is often a final verification step; in Islamic finance, compliance logic is the product logic. If the code permits even a single interest calculation, the entire transaction becomes religiously void. This level of criticality is rare in standard fintech.

The divergence stems from a fundamental philosophical shift regarding money. Traditional banking treats currency as a commodity that can be rented out for profit (interest). Islamic finance, conversely, views money merely as a medium of exchange. Profit can only be generated through trading tangible assets or sharing in genuine business risks. This transitions the financial model from debt-based to equity- or trade-based. Attempting to force a conventional core system to handle this is futile; these platforms must be constructed from the ground up with these distinctions at their core.

Core Pillars of Islamic Finance Platforms

1. The Prohibition of Riba (Interest)

The absolute ban on riba renders standard loan origination modules obsolete. Systems cannot automatically accrue interest over time based on a principal balance.

Instead of charging for the time value of money, the software must facilitate trade or leasing workflows. For instance, if a client wishes to purchase a vehicle, the bank (via the system) acquires the asset first and then sells it to the client at a marked-up price, payable in installments. The code must track the transfer of asset ownership rather than merely adjusting balance sheet figures. If your database schema assumes interest is a native field, future refactoring will be extremely difficult.

2. Profit-and-Loss Sharing Models

Without guaranteed interest, Islamic finance relies on shared risk. The bank and the customer become partners: profits are shared upon success, and losses are absorbed jointly if the venture fails.

Two primary models dominate requirements documents:

- Mudarabah: A silent partnership where one party provides capital (the bank) and the other provides labor and expertise (the entrepreneur). The software must meticulously track profit distribution ratios while also handling scenarios where no profit is generated. Unlike conventional loans where the bank is paid regardless of outcome, here the bank bears the financial loss if market forces cause failure. Coding logic for variable returns instead of fixed amortization schedules requires a completely different approach.

- Musharakah: A joint venture where both parties contribute capital and share management duties. The system must dynamically calculate returns based on actual performance and pre-agreed ratios. Since outcomes are less predictable than fixed-interest loans, reporting modules require significantly greater flexibility.

3. Asset-Backed Financing

Every transaction must be linked to a real, tangible asset. Speculative trading of paper instruments or derivatives (Gharar, or excessive uncertainty) is prohibited.

The architecture must maintain a clear audit trail connecting financial flows to underlying assets like real estate, vehicles, gold, or commodities. The system cannot simply move numbers between accounts; it must verify that an asset has changed hands or is under lease. This often necessitates integrations with inventory management systems or property registries, adding layers of complexity but providing a natural safeguard against speculative bubbles.

4. Ethical Investment Restrictions

Even if an opportunity is asset-backed and profitable, it is forbidden if it supports industries prohibited by Shariah. The software must include robust screening mechanisms to block investments in sectors such as:

- Gambling and betting

- Alcohol production or distribution

- Weapons manufacturing (particularly non-defensive types)

- Unethical activities (including conventional insurance with uncertain elements or pork-related products)

In many cases, these screenings must occur in real-time. If a fund manager attempts to invest in an entity deriving revenue from these prohibited sectors, the system must immediately flag or prevent the action.

Essential Capabilities of Shariah-Compliant Banking Systems

Specialized Islamic Product Management

Standard banking modules designed for generic "loans" or "savings accounts" are insufficient because these concepts do not translate directly to Islamic finance. Instead, the software must natively support specific Islamic contracts. Attempting to force these unique structures into traditional lending templates will quickly lead to compliance failures.

The system requires dedicated digital workflows for distinct contract types:

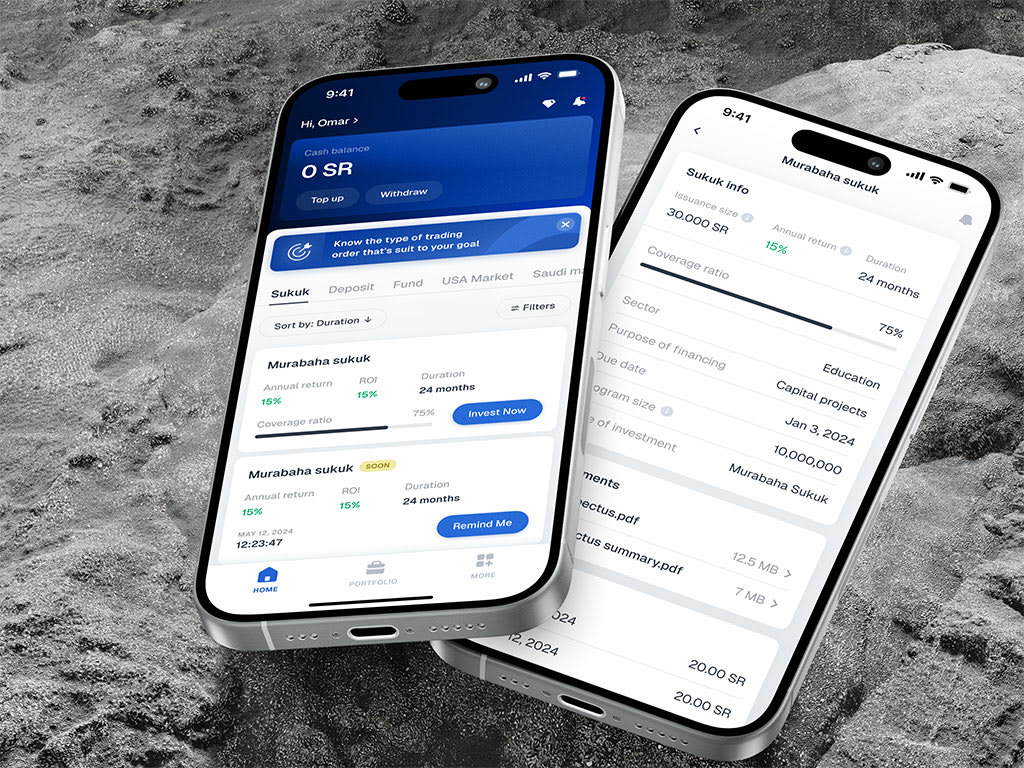

- Murabaha (Cost-Plus Financing): The platform must orchestrate a two-step sale process where the bank first acquires an asset and then sells it to the customer at a markup.

- Musharakah and Mudarabah: As previously discussed, these models demand engines capable of calculating variable profit distributions based on actual business performance rather than fixed interest rates.

- Ijara (Leasing): The software must manage the full lifecycle of asset ownership, lease payments, and the final transfer of title.

The most critical technical challenge lies in the state machine. A Murabaha transaction, for example, follows a rigid sequence: offer, acceptance, purchase, sale, and delivery. If the database logs show the purchase occurring before the acceptance, the entire contract is religiously invalid. While more complex than a simple "approve and disburse" flow, enforcing this strict order within the product module significantly mitigates legal and religious risk.

Compliance and Shariah Governance

In traditional banking, compliance aims to avoid regulatory fines; in Islamic banking, it ensures religious validity. Without this, the product holds no value for its intended users.

The architecture must include a dedicated governance module that facilitates digital review and approval by a Shariah advisory board. Beyond approvals, the system requires immutable, timestamped audit trails for every transaction. It must be able to instantly verify and report on key compliance questions: Was the underlying asset verified? Was the profit calculated without compounding interest?

Since manual verification is unscalable, real-time, AI-driven compliance monitoring is essential. Imagine a rule engine that automatically blocks a transaction the moment it detects an interest calculation or interaction with a prohibited entity. While developing such robust safeguards is demanding, it builds immense trust, allowing users to verify compliance with a single click.

Ethical Investment Screening

For wealth management or investment modules, relying on standard stock APIs is inadequate. The platform needs a sophisticated screening engine tailored to Shariah criteria.

This feature must filter potential investments not only by the company's primary business activities but also by financial health metrics, such as debt-to-equity ratios, to ensure the entity is not over-leveraged. The system must automatically exclude companies involved in prohibited sectors like gambling, alcohol, weapons manufacturing, or other unethical industries.

Furthermore, continuous portfolio monitoring is vital. Since corporate profiles evolve—a tech firm might begin heavy investment in interest-bearing bonds or acquire a non-compliant subsidiary—the platform must detect these changes immediately. It should either alert the user or automatically trigger a divestment process. Failing to include this dynamic monitoring is a surefire way to erode user confidence.

Payment and Transaction Infrastructure

The underlying payment rails must remain pure, ensuring end-to-end adherence to halal principles. Money transfers must never involve impermissible elements.

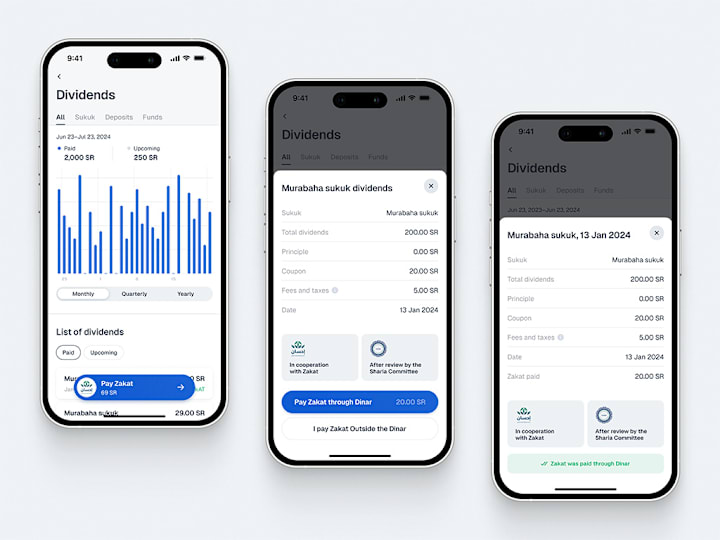

A notable complexity involves late payment penalties. Unlike conventional banking, where late fees generate income, Islamic finance may impose penalties to discourage delays, but these funds cannot be recognized as bank revenue. They must be segregated and donated to charity. The payment infrastructure must automate this logic, routing penalty funds directly to charitable accounts without affecting the bank's profit and loss statement. Overlooking this detail inadvertently generates riba (interest).

Additionally, deep integration with payment gateways capable of handling split payments and charitable routing is necessary. Since few off-the-shelf gateways support these nuances, developers often need to build custom connectors. While labor-intensive, this is crucial for maintaining a secure and ethically pure ecosystem.

Mobile and Digital User Interfaces

Robust backend logic is useless if the user interface is cumbersome. Modern users expect sleek, intuitive apps and will not tolerate legacy-style interfaces simply because the product is Shariah-compliant.

Platforms must be mobile-first, presenting complex financial products clearly. Imagine a dashboard offering real-time updates on a Musharakah investment, visualizing the split between capital contribution and profit share. Or consider a Murabaha tracker that explicitly shows the financing stage: "Bank Acquiring Asset," "Title Transferred," or "Installment Plan Active."

The key to success is translating complex concepts like "profit-sharing ratios" and "asset-backed leasing" into simple, actionable insights using plain language. Incorporating educational tooltips to explain why a transaction is structured a certain way can foster confidence. When users understand that extra steps exist to protect their faith, they appreciate the process. However, if the app feels clunky or confusing, they will abandon it.

The Development Lifecycle for Shariah-Compliant Banking Systems

1. Strategic Planning and Shariah Alignment

Before writing a single line of code, the financial architecture must be fully defined. You cannot simply decide to build a "home loan"; you must determine the specific Islamic contract structure, such as Murabaha or Ijara, as this choice dictates the entire technical roadmap.

This phase requires close collaboration with qualified Shariah scholars and compliance boards. Relying on internet research is insufficient; successful projects begin with joint workshops involving product leaders and religious experts to identify potential pitfalls early. For example, a scholar might flag that a proposed profit calculation inadvertently mimics compound interest. Identifying such issues during the planning stage prevents costly re-engineering of the core engine later. The objective is clear: validate that every product concept adheres to Islamic finance principles before translating it into technical specifications.

2. UX/UI Design Tailored for Islamic Finance

Once the logic is established, the focus shifts to design. This presents a unique challenge: Islamic contracts are often more verbose and complex than standard banking actions like "withdraw cash." The designer’s role is to distill this complexity into an intuitive experience without stripping away essential legal meanings.

Interfaces must guide users transparently through each contractual step. In a Murabaha flow, for instance, the UI should explicitly visualize the stages: "Customer Request," "Bank Acquisition," and "Resale to Customer." This transparency is vital for building trust; if the process appears opaque, users may suspect hidden interest charges. Clear language, clean layouts, and educational tooltips explaining the rationale behind specific structures are essential.

Additionally, development teams must account for localization, particularly support for Arabic and other right-to-left (RTL) languages. This often necessitates restructuring UI elements to ensure a seamless experience for diverse user bases.

3. Selecting the Technology Stack

Building these systems does not require obscure programming languages; standard enterprise stacks are highly effective when configured correctly.

- Backend: Java remains a top choice for large institutions due to its robustness and strict typing, which minimizes logic errors in financial math. Python (with frameworks like FastAPI) excels in speed and flexibility, ideal for data-heavy tasks like investment screening. Node.js is optimal for real-time features, such as pushing profit-sharing updates to users. C# (.NET) is still preferred for integrating with legacy banking infrastructure.

- Frontend: React and Vue are the leading frameworks for creating dynamic, interactive interfaces that can recalculate profit shares instantly without page reloads.

- Database: PostgreSQL is the safest option due to its strict ACID compliance, which is non-negotiable for maintaining accurate asset ownership trails. Redis should be employed for caching to handle the computational load of on-the-fly profit distribution calculations.

- Infrastructure: Containerization via Docker and orchestration with Kubernetes are critical for managing environments and scaling efficiently during high-traffic periods like Ramadan or Eid, ensuring system stability when transaction volumes peak.

4. Security and Compliance Architecture

In Islamic fintech, security and compliance are inseparable. Data integrity is paramount; if a transaction record is corrupted, it cannot simply be "fixed" later, as the religious validity of the transaction may be permanently compromised.

Compliance monitoring must be baked directly into the system architecture. Think of this as an always-on watchdog service that validates every transaction against a rule set in real-time. Did a trade involve a prohibited stock? Did a calculation accidentally apply an interest rate? The system must flag these anomalies instantly. This is especially crucial for blockchain-based implementations.

Furthermore, the system must generate immutable audit trails. Regulators and Shariah boards will demand a complete history of every action: who approved the contract, what was the asset value at the time of sale, etc. The database schema must support versioning and detailed logging by default. While setting this up is demanding, the inability to produce historical logs during an audit is unacceptable.

5. Ecosystem Integrations

No banking platform operates in isolation. Your system must connect seamlessly with the broader financial world, including other Islamic banks, payment providers familiar with halal flows, and specialized screening services.

Crucially, you must integrate with data feeds for commodity prices (gold, etc.) and stock market data. However, caution is required: many conventional data APIs include interest-based benchmarks by default. Developers must filter these out or source alternative data streams that align with Islamic principles. Constructing a digital payment infrastructure that respects these nuances requires extra effort but is essential for authenticity.

6. Testing and Shariah Certification

Standard software testing—unit, integration, and load tests—is merely the baseline. The defining step is formal verification by a Shariah advisory board.

Before launch, the software’s logic must undergo certification. Scholars will scrutinize algorithms, contract workflows, and edge cases. They might ask, "How does the system handle asset destruction before delivery?" If the code fails to address such scenarios in accordance with Shariah, the product is not ready for market.

Security audits are equally mandatory. Given that these platforms manage life savings, a breach could devastate confidence in digital Islamic banking. A comprehensive approach including penetration testing and rigorous code reviews is non-negotiable.

7. Deployment and Continuous Maintenance

Post-launch, the work continues. Monitoring must be continuous (24/7), looking not just for performance bottlenecks but also for anomalies that might indicate "compliance drift."

Compliance is dynamic; Shariah interpretations evolve, and regional regulations change. Your team must be agile enough to patch logic quickly—whether adapting to new permissible investment types or tightening screening criteria. The architecture must be flexible enough to accommodate these shifts without requiring a total system rewrite.

Obstacles in Building Shariah-Compliant Fintech Solutions

If developing this type of software were straightforward, major global banks would have mastered it long ago. While the market potential is enormous, the path is littered with unique pitfalls absent in traditional fintech. Even highly skilled teams often stumble here because they underestimate how deeply these challenges are woven into the legal and financial fabric.

1. The Precision of Religious Compliance

In standard digital banking, a bug that miscalculates interest by a fraction of a percent is a fixable operational error, often resolved with a refund. In Islamic finance, that same minor error can render an entire contract religiously invalid (haram).

The core difficulty lies in converting nuanced theological debates into rigid binary code. Scholars may spend weeks deliberating the specifics of a Murabaha structure; developers must then distill those conclusions into flawless if-else logic. Furthermore, these standards are not static. Interpretations evolve, and practices accepted five years ago may be scrutinized today. Consequently, systems must be architected for flexibility, allowing updates to ethical standards without breaking existing contracts. This means the definition of "done" is always shifting, requiring continuous validation against a moving target of religious ethics.

2. Retrofitting Debt-Centric Infrastructure

The global financial backbone—SWIFT, core ledgers, credit scoring—is fundamentally designed for debt and the time value of money (interest). Attempting to run asset-backed, risk-sharing models on this infrastructure is akin to driving a square-wheeled vehicle on a highway built for circles.

Consider commodity trading: many Islamic financing deals require the bank to physically purchase and instantly resell a commodity (e.g., palm oil or metals) to validate the transaction. Conventional APIs are not built for this rapid, back-to-back ownership flow; they expect simple debit/credit entries. Developers often end up building complex middleware just to simulate the legally required transfer of title. Similarly, traditional ledgers anticipate fixed liabilities. Coding a system that handles variable, performance-based returns necessitates a complete reimagining of the database schema. Patching old systems rarely works; often, parallel systems must be built, doubling the maintenance burden.

3. Embedding Governance into Code

In conventional fintech, compliance is often a retrospective monthly report. In Islamic banking, governance is a live, real-time process. The software must integrate the Shariah board directly into the operational workflow.

New features require digital sign-off from scholars before deployment, but the oversight doesn't stop there. The system must continuously monitor transactions to ensure they remain within approved parameters. If market shifts cause a fund to drift into a prohibited sector, the software must instantly flag or freeze the activity.

Creating this "digital scholar" layer is exceptionally difficult. It requires codifying human judgment and creating audit trails that satisfy both technical auditors (who want JSON logs and latency metrics) and religious scholars (who need proof of asset possession and intent). Bridging this linguistic and conceptual gap demands a backend and UX architecture that captures context, not just raw data—a feat standard compliance tools cannot achieve.

4. Navigating a Fragmented Regulatory Landscape

Adhering solely to AAOIFI standards is insufficient. While AAOIFI provides a general framework, local regulators in jurisdictions like Malaysia, Saudi Arabia, Pakistan, the UK, and Bahrain often enforce specific, sometimes contradictory, rules.

A product structure approved in Kuala Lumpur might require significant modification to launch in Riyadh due to differences in documentation or asset definitions. Global platforms therefore need a multi-tenant architecture where compliance rules are configurable by region. Additionally, regulatory reporting formats and metrics vary wildly by country. Keeping pace with these changes is a resource-intensive endeavor; many startups exhaust their capital manually adapting systems for each new market. The solution lies in abstracting the regulation layer as much as possible, though staying synchronized with global shifts remains a constant struggle.

The Strategic Value of Partnering with a Shariah-Compliant Development Firm

When reviewing budgets and timelines, engaging a specialized development partner might initially appear to be an unnecessary cost. However, Islamic fintech operates on a fundamentally different financial lexicon. Collaborating with a firm that possesses deep market immersion and specific expertise transforms the project from a high-risk experiment into a calculated success.

1. Mastery of Islamic Financial Models

Engaging generalist developers often results in weeks or months spent merely explaining core concepts like the distinctions between Murabaha and Musharakah. Even with training, there is a significant risk that their ingrained habits will lead to logic flows that inadvertently mimic interest-based structures—a common and costly error.

Specialized Islamic banking developers eliminate this learning curve entirely. They have already navigated these pitfalls, ensuring you don’t repeat them. They understand intrinsically that profit-sharing requires dynamic algorithms linked to real-world performance and that late payment penalties must be automatically diverted to charitable causes. This domain expertise prevents expensive post-launch refactoring, effectively paying for a product that is religiously valid from its first line of code.

2. Secure and Scalable Architectures

Building financial software is inherently complex; layering on asset-backed requirements and intricate contract states multiplies that difficulty. Standard banking architectures are insufficient for these demands. You need systems engineered to manage multi-step ownership transfers, real-time ethical screening, and immutable audit trails without compromising performance.

A specialized partner delivers architectures battle-tested for these exact scenarios. Their teams have already solved critical challenges, such as scaling a Mudarabah engine for thousands of concurrent users or ensuring commodity trades settle within the narrow timeframes mandated by Shariah. The result is a system that is secure by design and built for cross-border growth, capable of adapting to diverse regulatory environments without structural failure.

3. Navigating Global Regulatory Complexity

The regulatory landscape for Islamic fintech is a labyrinth. A model compliant in Malaysia may require significant adjustment for Saudi Arabia, while the UK offers its own unique interpretation. Attempting to navigate this alone risks launching a product that is legal in one jurisdiction but prohibited in another.

Experienced partners have already traversed this terrain. Having collaborated with Shariah boards across multiple regions, they possess a global perspective that accelerates time-to-market and minimizes friction. Engaging them is akin to hiring a guide who knows every shortcut and hidden trap, ensuring your expansion is smooth and compliant.

Final Thoughts

We have now reached the culmination of our journey. We began with abstract concepts like Murabaha and Musharakah sketched out on whiteboards, struggling to find their digital form. Today, those ideas have evolved into live, scalable solutions actively serving users every day.

If there is one essential takeaway, it is this: developing Shariah-compliant banking software is a delicate synchronization of technology and philosophy.

The process starts with the core tenets of Islamic finance: the prohibition of interest, the commitment to shared risk, and the tethering of finance to real assets. This foundational choice echoes through every phase of the project:

- Architecture: It drives the decision to build systems based on tangible asset ownership rather than mere monetary movement.

- Development: It ensures that every line of code adheres to strict ethical boundaries.

- Deployment: It results in a product grounded in integrity, not just profitability.

Ultimately, these platforms cultivate something rare: transparency and trust. When a user opens your application and sees precisely how their capital is deployed—confident that it is free from exploitation and prohibited industries—they develop a level of loyalty that no amount of marketing budget could ever purchase.

About the Creator

Shakuro

We are a web and mobile design and development agency. Making websites and apps, creating brand identities, and launching startups.

Locked Out of Your Email? The Complete 2026 Guide to Gmail Account Recovery and Security

Let’s be honest: your Gmail account isn't just an email account. It’s the master key to your digital life. It’s your YouTube history, your Google Drive full of documents, your saved passwords in Chrome, and the inbox where your bank statements and travel confirmations live.

By Alexander Hoffmannabout 9 hours ago in 01

I Replaced My 9-to-5 With ChatGPT

Eighteen months ago I was earning $45,000 annually as a marketing coordinator drowning in busywork and corporate politics, and today I earn $12,000 per month working twenty-five hours per week from my apartment using AI tools that handle eighty percent of the actual work while I focus on strategy, client relationships, and quality control, and the transition was not as difficult as you might think because most businesses desperately need people who understand both AI capabilities and human communication, and that intersection is where the money is.

By The Curious Writer2 days ago in 01

Comments

There are no comments for this story

Be the first to respond and start the conversation.